Shares of Protagonist Therapeutics (PTGX) have lost over two-thirds of their value year to date. The stock popped up on my radar after noticing several green flags, including institutional positioning and a key executive hire.

Chart

Figure 1: PTGX daily advanced chart (source: Finviz)

Figure 2: PTGX 15-minute chart (source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the first chart (daily advanced), we can see the huge gap down in March after negative clinical news was announced. In the second chart (15-minute), we can see the makings of a nice rebound underway with the stock likely to rebound at least to where it originally was above the $8 level.

Reader InquiryIn the marketplace service ROTY (Runners of the Year), we search for stocks that are attractive across multiple time frames with potential for high percentage upside within the near to medium term.

Late last week in ROTY, I published an update piece on an under the radar potential ASCO winner. A few days ago, in the model account, we added two key positions with catalysts coming up in the second half of the year.

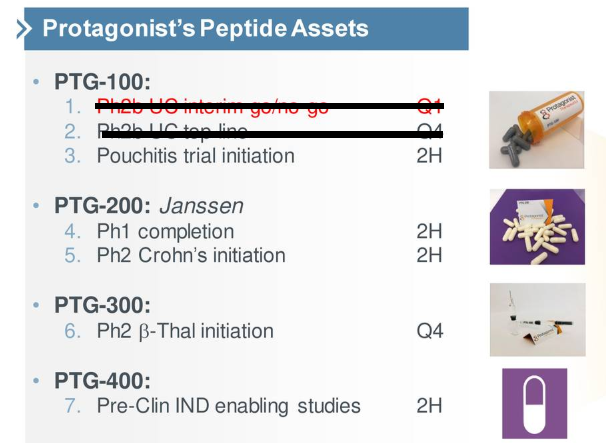

Figure 3: Pipeline (source: corporate website)

In the case of Protagonist Therapeutics, in ROTY Live Chat I pointed out several green flags to members yesterday. My objective now is to find out whether this one could rebound significantly in the near term and if it can potentially become our newest ROTY Contender.

Recent DevelopmentsThe stock price plunged in late March after the company announced disappointing news for their lead asset PTG-100, an oral GI-restricted alpha-4-beta-7 integrin antagonist peptide. In the phase 2b PROPEL trial, PTG-100 was being evaluated for use in patients with moderate to severe ulcerative colitis.

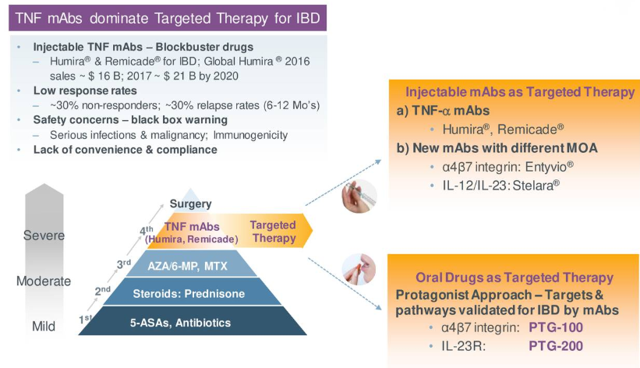

This was a potentially lucrative indication, a clinically validated target (multi-billion-dollar market opportunity) where an oral peptide would be a welcome alternative to injectable monoclonal antibodies. Treatments such as REMICADE and HUMIRA dominate targeted therapy for the IBD market with sales set to hit $21 billion by 2020. Unfortunately, setbacks such as low response rates, safety concerns, and lack of convenience represent major obstacles for such treatments. On paper, an investment in the company made sense, as their peptides held promise to address those obstacles and potentially transform the market by introducing targeted therapy to patients with mild-to-moderate disease and potentially being combined with other oral agents.

Figure 4: Blockbuster market opportunity snapshot (source: corporate presentation)

Unfortunately, the company announced discontinuation of the PROPEL study following an interim analysis by an independent Data Monitoring Committee of unblinded efficacy and safety data for the first 65 patients out of the 240 total the company wished to enroll. The DMC decided the trial wasn't worth continuing based on analysis of the primary endpoint of clinical remission. Importantly, there were no safety issues noted. However, a usually high placebo response was surprising.

As a result, the company also decided to postpone their decision concerning initiation of the phase 2/3 study in chronic pouchitis until after a full review of the interim data from the PROPEL study. Said review should be finished up in the third quarter.

If they do by chance decide to go ahead with the late-stage study, chronic pouchitis represents an attractive rare disease indication with around 20,000 patients in the United States and as many in Europe.

In mid-May, the company announced clinical and preclinical abstracts for PTG-300, their injectable hepcidin mimetic being evaluated for treatment of anemia and iron overload in rare blood disorders, had been accepted for oral presentation at the 23rd Congress of the European Hematology Association. The meeting takes place June 14th through the 17th and perhaps this catalyst could help the stock bounce back in the near term.

On May 24th, I came across two major green flags - one was the appointment of Samuel Saks, M.D., as Chief Development Officer. He will be in charge of the company's R&D efforts. It merits pointing out that prior he served in the same role at Auspex Pharmaceuticals until it was acquired by Teva Pharmaceuticals (TEVA) for $3.5 billion. He also was co-founder of Jazz Pharmaceuticals (JAZZ). Long-time ROTY readers will recall that key executive hirings are an indicator we keep close tabs on.

The news also just came out that Biotechnology Value Fund has acquired a 6.9% stake in the company (or rather raised their stake considerably). Interest by key institutional players is another green flag we look out for.

Other InformationFor the first quarter of 2018, the company reported cash and equivalents of $140.5 million, meaning their once promising platform is being valued at next to nothing currently. Management is guiding for an operational runway through 2019. Net loss for the period came in lower at $7.7 million while R&D expenses increased to $15.4 million. License and collaboration revenue totaled $10.8 million (revenue from activities performed under the Janssen Collaboration Agreement).

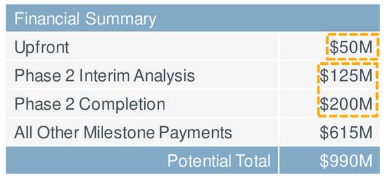

Speaking of which, the Janssen deal inked in May of last year merits highlighting. The collaboration is for co-development and commercialization of PTG-200, Protagonist's first-in-class, oral peptide IL-23 receptor antagonist. Keep in mind that Johnson & Johnson (JNJ) participated prior in a Series B financing for the smaller firm. Terms were attractive, with a $50 million upfront payment and milestones of up to $940 million (including significant development milestones for completion of the phase 2a/phase 2b study in Crohn's disease if Jansen chooses to keep its license after each event). Protagonist also is due double-digit tiered royalties on net product sales, later on, should they make it to approval.

Figure 4: Milestone breakdown from JNJ partnership (source: corporate presentation)

Dosing for all cohorts has been finished up in the phase 1 study in normal healthy volunteers (single-ascending and multiple-ascending doses). In the second half of the year, an IND filing in the US should pave the way for a global phase 2 study in Crohn's disease.

As for PTG-300 mentioned further above, an IND filing should be submitted in the third quarter to allow for initiation of a phase 2 study in beta-thalassemia patients in the fourth quarter. Later on, the company plans to explore other indications including treatment of anemia and transfusion-dependence in myelodysplastic syndromes and exaggerated erythropoiesis in polycythemia vera.

As for institutional investors of note, it's worth noting that EcoR1 Capital owns a new stake of over 1 million shares as well.

Final ThoughtsI'd like to close by referring back to BMO's analyst rating from early March, in which they placed an Outperform rating on shares and a $42 price target. The analyst stated the following (my emphasis in bold):

Low risk pipeline is quickly maturing with an interim analysis (futility) of the Phase 2b UC trial of PTG-100 later this month and final data in 4Q18. In addition, they expect advancement of PTG-200 into a Phase 2 Crohn's disease trial and start of PTG-300 trials in beta thalassemia in 2H18.

This is not to point fingers - I have my share of losers as well. It's to remind readers of two things, first that biotech is a minefield and the unexpected will happen from time to time. All we can do is manage risk the best we possibly can, so we'll be able to recover from such situations.

Secondly, other value drivers mentioned in that thesis are still intact for the latter two assets.

Perhaps after the steep decline, the present share price is an attractive entry point, considering the firm's cash position and insanely low valuation. In the near term, catalysts mentioned above could help to turn the situation around.

As for risks, there's always the possibility that the firm continues to burn cash without achieving success, resulting in further dilution down the road or worse. Nixing their lead program is possible, as is disappointing data and clinical setbacks (including delays) for their latter two programs or also the possibility of JNJ opting out.

I won't be adding this one to the ROTY Contenders List currently, as it merits more digging and I don't feel I have an advantage yet. That said, I look forward to coming catalysts and will continue to reevaluate. As stated before, the hiring of a high-profile executive and recent institutional positioning are two green flags to make this one worth following.

Keep in mind that when a stock is selected for ROTY, the corresponding article appears only to current subscribers. Also, for the purposes of due diligence, subscribers are able to access all of my archived work (getting around the 10-day paywall).

Disclaimer: Commentary presented is NOT individualized investment advice. Opinions offered here are NOT personalized recommendations. Readers are expected to do their own due diligence or consult an investment professional if needed prior to making trades. Strategies discussed should not be mistaken for recommendations, and past performance may not be indicative of future results. Although I do my best to present factual research, I do not in any way guarantee the accuracy of the information I post. I reserve the right to make investment decisions on behalf of myself and affiliates regarding any security without notification except where it is required by law. Keep in mind that any opinion or position disclosed on this platform is subject to change at any moment as the thesis evolves. Investing in common stock can result in partial or total loss of capital. In other words, readers are expected to form their own trading plan, do their own research, and take responsibility for their own actions. If they are not able or willing to do so, better to buy index funds or find a thoroughly vetted fee-only financial advisor to handle your account.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment